Renewable Heat Wave

Price is key. No matter the purchase, ultimately, if the price is right a customer’s inclination to make an investment escalates. This notion holds true when consumers consider their energy source options. Case in point, three years ago, the United Kingdom initiated an environmental program to support biomass-heat installations and other renewable heat sources through financial incentives. It opened a nondomestic renewable heat incentive (RHI) scheme for applications in November 2011, with a domestic RHI following last spring. The incentives created the right price for many consumers of biomass-heat that qualified under the nondomestic RHI in business, industry and public-sector organizations, and for homeowners, private landlords, social landlords and self-builders under the domestic option.

The RHI, which traces back to the 2008 Energy Act, was introduced in the legislation principally to help meet the U.K.’s goal of generating 15 percent of energy from renewable sources by 2020, as set out in the Renewable Energy Directive. The government has identified indicative contributions of renewable energy from the electricity, heat and transport sectors that would allow the U.K. to meet the overall target as cost effectively as possible. The Department of Energy and Climate Change identified that for heat, up to 12 percent could be generated from renewable sources by 2020, increasing from the approximate 2 percent reported in December.

Although the RHI supports the installation of renewable energy technology other than biomass, biomass plants have achieved the quickest rate of uptake. Other incentivized technologies for both residential and commercial consumers include air-source and ground-source heat pumps and solar thermal systems, and in the commercial sector, water-source heat pumps, deep geothermal plants, biomethane production for injection and biogas plants. Consequently, the uptake has had a sizeable impact on the supply and demand for many of the plants’ sources of fuel, pellets and wood chips. “The renewable heat incentive has caused the wood heating industry to explode in a way nothing else prior to that and probably subsequent is going to,” says Julian Morgan-Jones, Wood Heat Association chairman and managing director of South East Wood Fuels Ltd.

South East Wood Fuels transports predominantly wood chips and some wood pellets to commercial and institutional wood heating customers in the South East and London. The industry has grown from about 50,000 tons of A1-grade pellets in 2010 to 240,000 tons projected in the current year, according to Bruno Prior, managing director of Forever Fuels Ltd., a wood pellets supplier in the U.K., and a board member of the WHA with Morgan-Jones. Neil Harrison, co-founder of re:heat and WHA vice chairman, says the RHI is “probably the most generous renewable energy support scheme, if not in Europe, probably in the world, at the moment.” He adds, “The economics are very strong for biomass as a result.”

The RHI can be regarded as one of the key reasons there was a need for the association. “The WHA is there to grow and maintain the wood heating industry in the U.K., and to also do work to improve standards and improve the reputation of the industry,” Harrison says.

The WHA falls under the umbrella of the Renewable Energy Association, which was instrumental in lobbying for the RHI scheme. There was a need for an association that reflected the specific needs of the wood heating industry, Morgan-Jones says. Now, 140 representatives from various companies are members of the association.

While the WHA helps support the wood heat industry as it grows under the RHI, the Office of Gas and Electricity Markets (Ofgem) serves as policy administrator. Ofgem E-Serve publishes guidance materials, receives and assesses applications, makes payments to approved applicants, ensures ongoing compliance with scheme rules and provides quarterly and annual public reports.

Each RHI scheme has its own tariffs, but similar conditions, rules and application processes. Applicants must fill out online applications under both schemes. Installations for the nondomestic scheme are provided subsidies payable for 20 years to eligible renewable heat generators. These tariffs are available at a different rate depending on the size of the boiler. The tariff levels for boilers up to 999 kilowatts (kW) are based on a two-tier payment structure: tier-one payments up to 1,314 peak load hours of operation (15 percent annual heat load) and tier-two payments for operational hours above this. This tariff structure operates on a 12-month basis, starting with the date of accreditation or its anniversary. Small biomass boilers up to 199 kW receive 6.8 pence (p) (10 cents) per kWh for tier one and 1.9 p per kWh in tier two. These tariff rates will be revised on April 1, 2015. The eligible-sized medium biomass boilers between 200 kW and 999 kW receive a tier -one payment of 5.1 p per kWh and 2.2 p per kWh for tier two. A single tariff level of 2 p per kWh is available for boiler capacities of 1,000 kW and above.

The residential RHI has a single tariff of 12.2 p per kWh, payable quarterly for seven years, although a recent reduction in the tariff to control the budget, or degression, decreases the payment to 10.98 p per kWh for applications submitted after the first of the year. The biomass technology covered includes biomass-only boilers and biomass pellet stoves with integrated boilers. Although there is no limit on the capacity of the product, it must be certified by the Microgeneration Certification Scheme or an equivalent scheme. Besides this certification, the renewable technology must be listed as eligible on the Product Eligibility List, have an Energy Performance Certification for the property and meter the heating systems to receive payments in certain situations, among a number of other credentials. RHI applicants for both schemes must also be below certain emission levels. As of September 2013, all applicants with a biomass boiler are required to submit an RHI emission certificate or environmental permit. The maximum levels for biomass boilers are equal to 30 grams (g) per gigajoule (GJ) particulate matter (PM) and 150 g per GJ nitrogen oxide (NOx).

Doubling The Industry

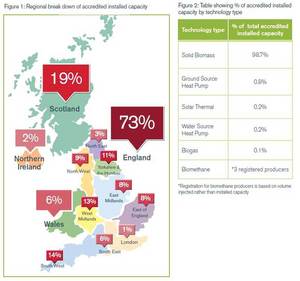

There is no denying that biomass installations have risen above other renewable energy technology covered by the RHI. According to a recent Ofgem E-Serve quarterly report, 7,258 installations are accredited in the nondomestic scheme and more are expected. Between September and December 2014, 1,203 new, full applications and three preliminary applications were accredited, or an increase of 130 percent since the same quarter in 2013. These installations and other RHI technologies amount to over 1 gigawatt (GW), which was the reported installed capacity as of Aug. 15 last year. Even with the exclusion of residential applications until last year, around 6,500 biomass installations have been approved as of mid-February, according to Ofgem accreditation reports.

DECC releases forecast expenditures on a monthly basis based on data provided by Ofgem. DECC estimates the cost of RHI payments over the 12-month period following the assessment date, which assumes that all installations that were accredited or had registered full applications by that date would receive payments from the start of that 12-month period. As of Dec. 31, £153.6 million (British Pounds) ($236.7 million) is the forecast expenditure for all nondomestic biomass applications, including combined-heat-and-power systems. Small boilers up to 199 kW account for £110.5 million of the forecast amount. The total forecast expenditure, i.e., expenditure for the scheme as a whole over the next 12 months, is £270.4 million. Biomass leads all other technology with these budget commitments by a ratio of 19 to 1, truly proving dominance within the scheme. A similar theme can be found in the residential market, with total forecast expenditure for biomass plants as of Dec. 31 at £17.02 million, a staggering comparison to the combined total of £3 million for all other technology under the domestic RHIs.

Increased expenditures to biomass installations have naturally translated into growth in the wood fuel industry. Edward Billington grew his pellet distribution business, Billington Bioenergy, over the years, and now it has recently been acquired by the Drax Group. This partnership resulted as Drax hopes to help transform the U.K. heat market in the same way they’ve transformed the power market. Billington believes this opportunity will help develop the marketplace for the long term. Billington estimates that Billington Bioenergy serves about 2,000 approved RHI applicants. “We have seen a good uplift in the industry this winter, with a good number of installations going in, both domestic and nondomestic,” Billington says. “The growth has been encouraging, and certainly manageable to date. However, it has been so slow in starting, and coming from such a small starting point, that the U.K. needs to sustain these growth rates at least for the next few years, or even to accelerate them a bit more, to build a truly sustainable wood pellet industry in the U.K. for the long term.”

A pellet producer in the space, Verdo Renewables Ltd., has pellet plants in Andover in Hampshire and Grangemouth, Scotland. Each U.K. plant has the capacity of 55,000 metric tons of wood pellets and 15,000 metric tons of wood briquettes per year. Richard Smith, managing director at Verdo and chairman of the U.K. Pellet Council, agrees with Billington in that the RHI has started to have a considerable impact this winter. “It’s really shown that the demand for pellets has grown dramatically,” he says.

Smith adds that everybody has seen significant growth, and although they haven’t finalized their numbers, they estimate that “the demand in 2014 was just under 150,000 tons, and demand in 2015 will be upwards of 300,000 tons.” Smith says, “Roughly, the sector has doubled for purely heating pellets, this does not include cofiring pellets at power stations.”

Policing The Cowboys

Upon the onset of winter, biomass boiler installations are increasing at a fairly rapid rate, perhaps even too rapidly for the industry to keep up. Billington alludes to a potential concern when he says the growth needs to be sustained. Harrison’s business, re:heat, provides a wide range of services to the biomass heat market. A lion’s share of the business is the distribution of boiler equipment, but lately the company has been doing a lot of consultancy and remedial work for customers who have been left with an installation that isn’t working properly. “There is a growing body of that type of stuff, unfortunately, which is why we need to work together as an industry to put together proper standards and police the cowboys,” he says.

Cowboys in the U.K. are people, generally contractors, who don’t do a proper installation job. “As one might expect, a rapidly growing industry brings its own challenges in terms of available skills and expertise and problem resolution processes,” Morgan-Jones says. “Currently there are a fair number of poorly conceived and implemented boiler installations and so we’re getting customers who have problems. The WHA is looking to help standards and training for all parts of the supply chain to improve this and maintain the reputation of the industry. Equally, installers and fuel suppliers need to learn how to work together to determine the cause of problems and solve them rather than blame each other. At the end of the day, we all need happy customers.”

Solving these problems is one of the three core objectives of the WHA to meet in this year and beyond, Morgan-Jones says. The first objective is funding––the government funding for the RHI is committed only until March 2016. The U.K. has an upcoming election in May, so it is essential for the industry to get the best possible deal from the new government for the RHI beyond this point. The second objective is to raise awareness about the WHA, and promote wood heating to a larger audience in the marketplace. The third big focus is quality and standards. “We need to professionalize the industry, make sure we have the right training and best practices, and do it effectively,” Morgan-Jones says.

Harrison believes the real crux of the issue is that biomass heat is still fairly new technology in the U.K. He recalls just five years ago he could name most of the companies and individuals in the space, and now there are new companies entering the industry almost every day. “They don’t always enter it with the right level of skills and knowledge to actually execute a successful project, so that is a critical issue,” he says. “It doesn’t take a rocket scientist to work out the kinds of things that can happen when you have lack of barriers to entry, low-skill levels and a very generous tariff support regime.”

Another critical issue is the disproportionate awarding of funding. Prior says, the RHI has encouraged the installation of many small biomass boilers, but there are many things that need to be done to improve the program. “We have a very cost-effective technology that is being encouraged in some ways cost ineffectively,” Prior says.

For example, a critical issue is the disproportionate awarding of funding to sub-200 kW boilers (furnaces), which creates unintended consequences, encouraging boilers to be both oversized and undersized for the requirement leading to inefficiencies and/or under-powered systems.

He adds that even if the budget is extended after the upcoming elections, it will only be available for a few more years. “Beyond that, we are going to need to be pretty cost competitive, because we’re not going to be in the same world of generous financial subsidies,” Prior says.

Yet another challenge with the RHI is the the tension between the need for change in the future and the fear of change in the future, creating uncertainty amongst potential applicants. “The RHI could be improved after the general election,” Prior says. “However, the new government will need to strike a careful balance between correcting the worst failings in the design, and creating further uncertainty and complexity that inhibits investment. There is no time to be lost if the U.K. is to get anywhere near its 2020 renewable heat commitments.”

Billington believes changing the program has made it difficult to understand for some. “My personal opinion remains that it was too complex, and the rules were altered and tinkered so much that few truly understood it or could trust in its development,” Billington says. “Had they made it simpler and made a clearer commitment to it, then it would have been better understood and more effective, and you might have achieved more at a lower cost. Hence, it is crucial now that they don’t keep tinkering, but rather allow the policy to settle down and have a stable run for the time being.”

Some changes coming this year will impact biomass installations. One change is degression, which, according to Prior, has been 30 percent over the past 12 months. One big change in autumn, subject to parliamentary approval, is associated with government plans to introduce sustainability criteria for using biomass fuels. The easiest way for applicants to comply with the criteria will be to source an approved fuel from the Biomass Suppliers List, a pre-approved list of fuel suppliers.

An Unknown Future

The stability of the program is called into question with policy stagnation due to the election in May, not to mention current low oil prices. “It is crucial that they come back to seeing the bigger picture for the election, that biomass heating represents a sensible and sustainable alternative to using fossil fuels, improves our energy security, and that the RHI represents good value for money to develop this technology quickly in this country,” Billington says.

Another question is whether there will be an opportunity for North American producers to take advantage of the growing market. The schemes have clearly created the opportunity for expansion in the U.K. wood-heat industry, but when it comes to the U.S., as one of U.K.’s largest biomass suppliers for industrial power, the opportunity is less clear. Based on conversations with players in the industry, the general sentiment is that the opportunity isn’t there at the moment, but could certainly be in the future. This potential opening for U.S. producers seems to circle back to “if the price is right, then the opportunity is there,” Harrison says.

Billington thinks that North America’s involvement will become very important and actually help make the U.K. market fully robust and sustainable. “The key, however, is to get the quality right,” he says. “Achieving the EN-plus quality standard fully and consistently is more difficult than it might initially appear, especially when transporting over distances. The U.K. producers have done a superb job at this, and very much set the level which others must achieve.”

Smith with Verdo Renewables says that there is still a mindset change that North American producers must make to hit the U.K. heat market. “They are used to supplying large shiploads to power stations, and the power stations are traditionally near ports, and have significant dock sites,” he says.

Smith adds that the distribution network in the U.K. is significantly smaller than the power-pellet demand, so there is a limited ability to import 15,000-metric-ton shipments and store the pellets. The financial cost to ship is high for the still relatively small market, and the quality of the pellet once it arrives is not always ideal in terms of fines, which is probably the main challenge for U.S. and other exporters targeting the U.K. market.

Time was needed for the RHI to make an attention-worthy impact, but now that it is catching hold, people in the industry hope funding can continue until at least the end of the decade to help create a sustainable market for the future. “There is a certain amount of inertia in getting these markets to move,” Morgan-Jones says. “The RHI has done this, but it has taken a while for the momentum to build, and now that it has we need to ride the wave while it’s here. That wave could go flat on the beach if the budget is not supported beyond 2016 and it would be a huge shame not to use this momentum to achieve the government’s carbon reduction targets for 2020. My hope is certainly that for the next four years the wave continues to grow until it hits the beach in 2020, and then the hope there is that by 2020 there is some other scheme in place to be able to make sure it is sustainable on an ongoing basis.”

Read More: Wood Fuel Boilers